To differentiate contra entries from other entries, letter “C” is printed in the posting reference column (on both the debit and credit sides of the cash book). The only exception is that a column is added in a three column cash book to account for bank-related transactions. It acts as a journal or book of prime entry because all cash transactions are recorded in it as and when they take place. Goods purchased on credit from Sam, list price $ less 5% trade discount.

Step 4 – Calculating the Cash Balance Carried Down and Balance Brought Down

- A cash book is set up as a subsidiary to the general ledger in which all cash transactions made during an accounting period are recorded in chronological order.

- A contra entry is when an entry is made on the debit side and the same entry is recorded on the credit side of the cash book.

- It contains debits and credits which are double-entry Bookkeeping entries.

- 11 Financial is a registered investment adviser located in Lufkin, Texas.

This version has other detailed information, such as purchase or sales discounts, in addition to the information found on the single- and double-column cash books. Users often use some form of accounting software to manage the triple-column cash book. A contra entry is when an entry is made on the debit side and the same entry is recorded on the credit side of the cash book. A bank account may have an overdrawn balance because by arranging an overdraft with the bank, it is possible that more money may be withdrawn from the bank than what was deposited. If the debit column is larger than the credit column, the difference represents cash at bank.

Recording Transactions in a Cash Book

The business received a further cash discount of 10% for prompt payment. The petty cash book may be considered to be a fourth type of cash book. The bank cash book is a type of cash book that is used to track the transactions between a business unemployment and its bank. The main differences between a cash book and a pass book are how they track payments in cash and receipts, and who tracks them. A cash book format will track all of the money that is deposited and withdrawn from the account.

Cash Book and Bank Statement: Explanation

This is the reason why discount columns are also provided in the cash book. The source of cash book entries are deposits received from banks, cheques issued to creditors. When an account holder issues a cheque, which the bank pays, the bank debits the account holder’s personal account. The balance of the cash book is included in the trial balance like a regular ledger account.

Advantages of Cash Books

When an account holder deposits money with the bank, the bank’s liability to the account holder is increased from the bank’s point of view. Cash books are important because their proper maintenance and reconciliation with bank statements are fundamental for a business. By maintaining this book, businesses can have a clear, detailed, and organized record of all their financial activities, making financial management efficient and straightforward. Jami Gong is a Chartered Professional Account and Financial System Consultant.

11 Financial is a registered investment adviser located in Lufkin, Texas. 11 Financial may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. The letter “C” indicates that the contra effect of this transaction is recorded on the opposite side.

If a check is issued to a supplier, an entry is created in the bank column on the credit side of the cash book. Businesses use cash books to remain aware of their position with banks, while banks maintain records to ensure their position with an account holder is known. Journals are descriptive financial records of a business used for future reconciling.

Every time cash, checks, money orders, or postal orders (or anything else) are deposited in the bank, the cash book (bank column) is debited. That’s to say, an entry is made in the bank column on the debit side of the cash book. The cash book is maintained in the form of a ledger account, where receipts are put on the debit side and payments on the credit side.

This type of cash book is mostly used by individuals who are tracking their personal finances. To differentiate contra entries from other entries, letter “C” is printed in the posting reference column (on both the debit and credit sides of the cash book). Bank charges are recorded on the credit side of the cash book in the bank column.

It has debits and credits, which are double-entry bookkeeping entries. On the other hand, credits show decreases in value or liability accounts. In the general ledger, two separate accounts are maintained for discount allowed and discount received. Most business owners today use accounting software to maintain books. However, knowing how to balance a cash book is still beneficial.

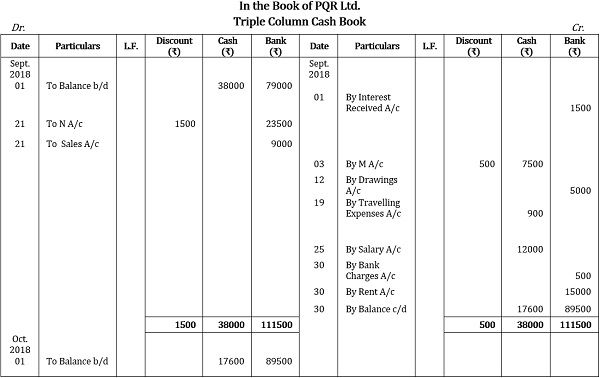

P&G LLC records its cash and bank transactions in a triple-column cash book. An overview of this procedure is given on the double column cash book page. A cash book contains receipts and payments of cash, credit sales, etc. It will show the date of the transaction, name of the customer (if any), account to be debited (positive amount) or credited (negative amount).